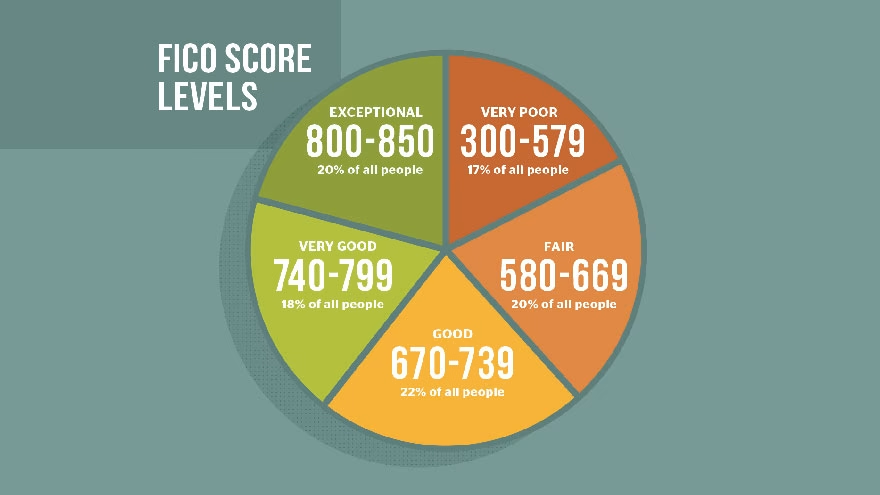

- about 90 percent according to the Fair Isaac Corporation -

- use the FICO scoring model when making credit decisions. There are three ways get an actual or estimated FICO score, none of which involves responding to “free” credit score offers on personal finance websites.

You can get a free score if your lender or credit card company participates in the FICO Open Access program, you can purchase it, or you can use the MyFICO score estimator.

Fico Open Access Program

The Fair Credit Reporting Act makes it easy to get a copy of your credit report once every 12 months from each of the three credit agencies. However, credit reports don’t include your credit score by default, and the law doesn’t require reporting agencies to provide your credit score.To remedy this, the Fair Isaac Corporation started the FICO Open Access program in November 2013. The program offers credit card companies and lenders the opportunity to give customers their FICO scores free of charge. As of January 2020, participating companies -

- including Bank of America, J.P. Morgan Chase, Ally Bank, Discover, Barclays Bank, First National Bank of Omaha and Sallie Mae -

- provide free FICO to some or all of their customers.

Purchasing a Fico Score

The traditional way to get a FICO score is to purchase it in combination with a copy of your credit report. For example, FICO and Experian offer the option to purchase a copy of your credit report from one or all three agencies, Equifax offers an official FICO score only in combination with an Equifax credit report and TransUnion offers a proprietary version of a FICO score as part of a credit monitoring membership program.

The Fico Estimating Tool

If you don’t need your actual score, the FICO estimator is a free tool that can aid you gauge your score. The tool asks 10 questions about credit card and loan balances, payment history and negative credit events such as judgements and repossessions. The result is a 50-point range in which your FICO score likely falls.You Might Also Like :: How to Calculate Coverage for Renter’s Insurance

Patrick Harwood

Patrick Harwood has been a professional writer and editor since 2004, specializing in articles about spectator sports, personal finance and law. He has contributed to family of magazines and websites.

Leave a reply

Replying to