Who Pays Estimated Taxes After a Person's Death? The short answer is that the deceased person no longer makes future estimated tax payments, but taxes already owed still have to be handled. The final individual income tax return, estate income tax return, and estate tax questions are separate.

This is general legal and tax information, not legal or tax advice. State law, filing status, estate income, trust terms, and court authority can change the answer. A personal representative should speak with a CPA or probate attorney before paying or skipping tax payments.

Start With The Final Return

The final Form 1040 reports income through the date of death. A surviving spouse may file jointly if eligible, or the personal representative may file for the deceased person. Any balance due is paid from the deceased person's funds or estate assets, not from a volunteer relative's pocket unless that person is legally responsible.

The IRS page for a deceased person explains that final income tax returns and estate income tax returns are separate responsibilities.

Estimated Payments Stop

A deceased taxpayer is not expected to keep making future estimated tax payments after death. The issue becomes whether enough tax was paid for income earned before death and whether the estate itself earns income after death.

Do not keep sending quarterly vouchers automatically without asking the tax preparer what period the payment covers.

Estate Income Is Different

After death, income from estate assets may belong on Form 1041, the estate income tax return, if filing thresholds are met. Interest, dividends, rents, business income, or capital gains after death may belong to the estate or trust, not the final Form 1040.

IRS guidance on estate income tax returns separates the final personal return from the estate's return.

Who Has Authority

The personal representative, executor, administrator, or trustee usually handles tax decisions. A family member with no authority should not write checks from estate accounts. Court appointment, trust authority, or spouse status matters.

Livecub's probate court basics can help families understand how court authority fits into estate administration.

Use Estate Funds

Taxes owed by the decedent or estate are usually paid from estate or trust assets before distributions. If the estate lacks cash, the representative may need to sell assets, wait for income, or ask the court or adviser about priorities.

Do not distribute all cash to heirs and then discover tax bills remain.

Refunds

If the final return shows a refund, the surviving spouse or representative may claim it. The IRS may require Form 1310 in some situations. Keep appointment papers and proof of authority with tax records.

If death records are still being gathered, Livecub's death certificate search guide can help families understand document steps.

Joint Returns

A surviving spouse may be able to file a joint return for the year of death if they have not remarried before year-end and other requirements are met. Estimated payments made before death may apply to that joint return.

A joint return can change tax, refund, and signature issues, so do not assume separate filing is best.

State Estimated Taxes

State estimated tax rules can differ from federal rules. Some states have separate final return, estate, inheritance, or fiduciary income tax procedures. Check the state revenue department.

A federal answer is not always a state answer.

Penalties

Underpayment penalties may still be considered if too little tax was paid before death. A preparer can check safe harbor rules, withholding, prior-year tax, and timing. Death does not automatically erase every tax calculation.

Good records of payments and withholding make this easier.

Medical And Deduction Timing

Final medical expenses, property taxes, and other deductions may be handled in more than one possible way depending on facts. Some expenses may affect the final return, estate return, or estate tax return. A CPA should coordinate this.

Do not categorize large expenses from memory.

Inheritance Tax Confusion

Estimated income tax is not the same as estate tax or inheritance tax. Estate tax looks at transfers at death. Inheritance tax, where it exists, may apply to recipients. Income tax looks at taxable income.

For related estate planning context, Livecub's credit shelter trust article can help explain one planning tool.

Keep A Tax File

Save W-2s, 1099s, brokerage statements, estimated tax vouchers, prior returns, death certificate, court letters, and estate account statements. A clean file prevents duplicate payments and missed income.

Taxes after death are easier when the representative is organized.

Before Paying Anything

The representative should identify exactly which return the payment belongs to. A final Form 1040 balance, a fiduciary income tax payment, an old estimated voucher, and a state notice are not the same thing. Paying the wrong account can create refund delays, notices, or arguments among heirs.

Match every payment to a tax year, taxpayer identification number, return type, and source of authority. If the estate has a new employer identification number, do not casually use the deceased person's Social Security number for post-death estate income.

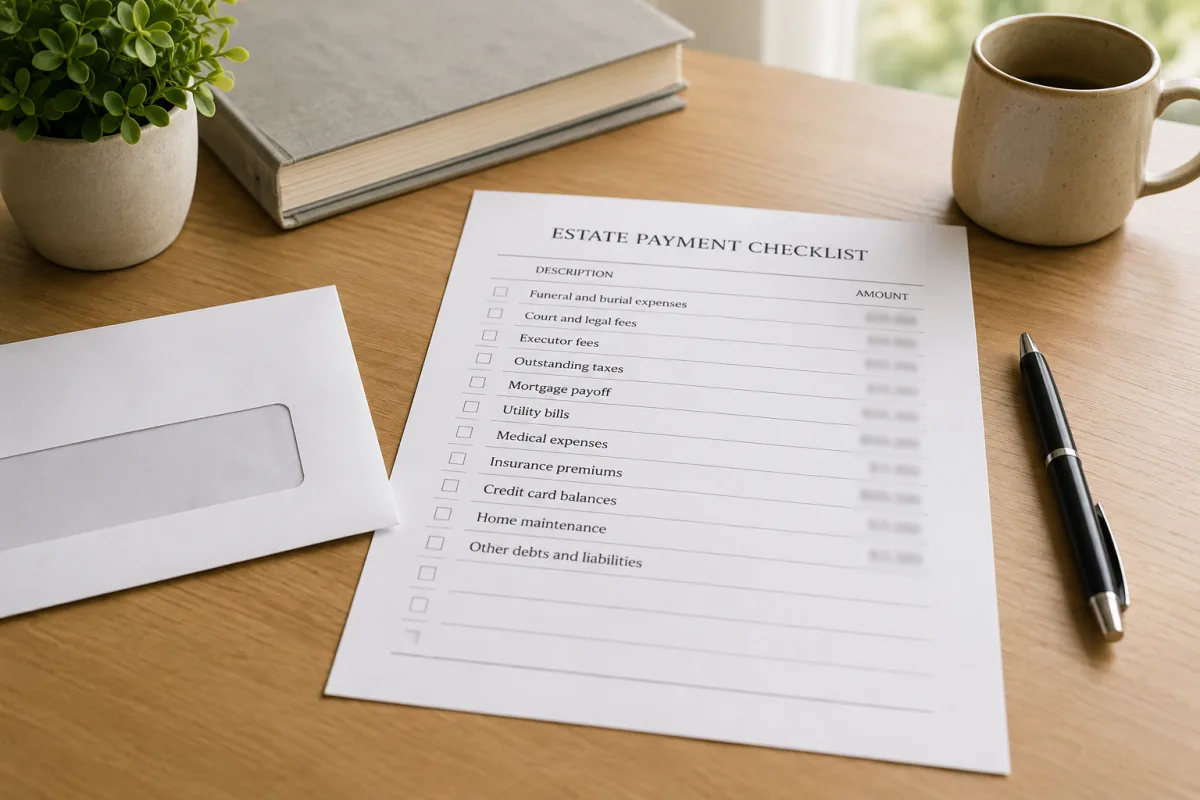

Cash Flow And Priority

Estate bills often arrive in an uncomfortable order. Funeral costs, mortgage payments, insurance, utilities, medical bills, credit cards, tax notices, and administration expenses may all compete for the same cash. Taxes can be high-priority debts, but local probate law may set exact payment order.

That is why early distributions are risky. A representative who distributes money too quickly may have to ask beneficiaries to return funds or may face personal exposure under state law. Hold a reserve until the tax preparer has reviewed likely income, deductions, and filing duties.

What To Ask The Tax Preparer

Bring prior-year returns, current-year income forms, estimated tax receipts, brokerage year-end statements, real estate closing papers, and bank statements showing income after death. Ask which returns are needed, which taxpayer number applies, who signs, and when payments should be made.

Also ask whether safe harbor rules, withholding, or prior estimated payments reduce penalty risk. The answer may depend on whether a joint return is filed, how much income arrived before death, and whether the estate earned enough income to require its own return.

When A Trust Is Involved

A revocable living trust may become irrevocable at death, and its income reporting may change. The trustee may need a new tax identification number, fiduciary return, or accounting. Trust ownership can also affect who has practical access to the money used for tax payments.

Do not assume the probate executor controls trust assets. If a trustee and executor are different people, they should coordinate records and deadlines so income is reported once, deductions are not missed, and payments come from the correct account.

Notice Handling

IRS and state letters should be opened, scanned, and sent to the preparer quickly. A notice may be routine, but deadlines still matter. Keep the envelope, because mailing date can matter when calculating response windows.

If the notice names the deceased taxpayer, the estate, a trust, or a surviving spouse, note that distinction before responding. A short call to the wrong department can waste weeks, while a properly signed response with authority papers can clear the issue faster.

If A Payment Was Already Sent

If someone already mailed an estimated payment after death, do not panic. Save proof of payment, check whether the check cleared, and ask the preparer where the payment was applied. The payment may be credited, refunded, or moved, depending on the account and timing.

The worst response is sending a second payment without understanding the first one. Duplicate payments can tie up estate cash and make accounting harder for beneficiaries.

Heir Communication

Beneficiaries do not need every tax detail, but they should understand why money is being held back. A short written update can explain that final income tax, fiduciary income tax, state tax, and possible notices must be resolved before full distribution.

Clear communication reduces pressure on the representative and creates a paper trail showing that tax reserves were a deliberate administration step, not delay for its own sake.

Frequently Asked Questions

Does a deceased person keep paying estimated taxes?

No future personal estimated payments are usually required, but final tax and estate income tax may still be due.

Who pays the final tax bill?

The personal representative usually pays from estate assets, subject to state law and priority rules.

Is estate income taxed separately?

Often yes. Income earned after death may require an estate or trust income tax return.

Can a surviving spouse file jointly?

Sometimes, if requirements are met. A tax professional should check.

Should heirs pay from personal funds?

Not unless legally responsible. Taxes are usually handled through estate administration.

The Practical Takeaway

After death, future personal estimated payments usually stop, but the final return, estate income tax, state tax, refunds, and payment priority still need careful handling by the authorized representative.

Tory Stearns

Edits practical household, travel and lifestyle explainers. Claims that can change are linked to current primary or subject-authority sources.

Leave a reply

Replying to