Children absorb far more from a grocery aisle than from any lecture about saving. They watch which items go back on the shelf, how adults react to a surprise bill, and whether a promise to wait for a sale actually holds. Money habits form in those ordinary moments, which is good news: you do not need a finance background to raise a capable spender, only a willingness to make everyday choices visible.

This is financial education, not personalized advice. Family income, culture, custody, and local laws shape what fits, so use the ideas that suit your child and ask a professional before any legal, tax, or investment decisions.

Match the Lesson to the Age

The fastest way to frustrate a child is to teach a concept their brain is not ready for, like compound interest to a five-year-old or coin-sorting to a teenager. Skills stack in a rough order, and each stage builds on the last. The table below is a map, not a schedule; children move at their own pace.

| Age range | Core skill | Good tools |

|---|---|---|

| 2-4 | Money buys things; we choose | Coins for sorting, pretend store, simple choices |

| 5-7 | Saving, spending, waiting | Spend/save/give jars, small short-term goals |

| 8-10 | Earning and tradeoffs | Price comparison, receipts, small allowed mistakes |

| 11-13 | Budgets and values | A real mini-budget, ad and in-app awareness |

| 14-18 | Real-world practice | Pay stubs, bank accounts, credit basics, scams |

Early Years: Choices, Jars, and Waiting

Very young children can grasp that money buys things and that choosing one item means skipping another. Use coins for sorting, a pretend store, and plain language: "We are buying apples today, not cookies." Calm repetition beats explanation. The Consumer Financial Protection Bureau's Money as You Grow program reassures parents that you do not need to be an expert to build these habits.

By ages five to seven, three containers, spend, save, and give, make the abstract concrete. Keep amounts small and visible, since physical coins show money leaving and growing in a way digital numbers cannot. Let them save toward a goal that takes a few weeks, not a year; a distant goal teaches frustration instead of patience.

Middle Years: Earning, Tradeoffs, and Budgets

Between eight and ten, children can connect effort, time, and money. They can compare prices, read receipts, split birthday money, and feel that spending on one thing means waiting on another. Let them make small mistakes while the stakes are low. The FDIC's Money Smart for Young People offers caregiver guides with activities on saving, goals, and online safety that fit this curiosity well.

Middle schoolers can help plan part of a real budget: school supplies, sports gear, a party, or clothing within a set amount. Give the number, explain the priorities, and let them compare options. Handing over a fixed clothing budget for a school year, for example, teaches more about tradeoffs in one season than a dozen reminders to be careful with money. When the total is theirs to manage, the choice between one expensive item and several cheaper ones becomes real rather than hypothetical.

This is also the age to talk about advertising, in-app purchases, subscription traps, and influencer pressure, because a child who understands why something is tempting has a better chance of slowing down before buying. Point out how a game is designed to make spending feel small, or how a "limited time" banner creates urgency, so the persuasion becomes visible instead of invisible.

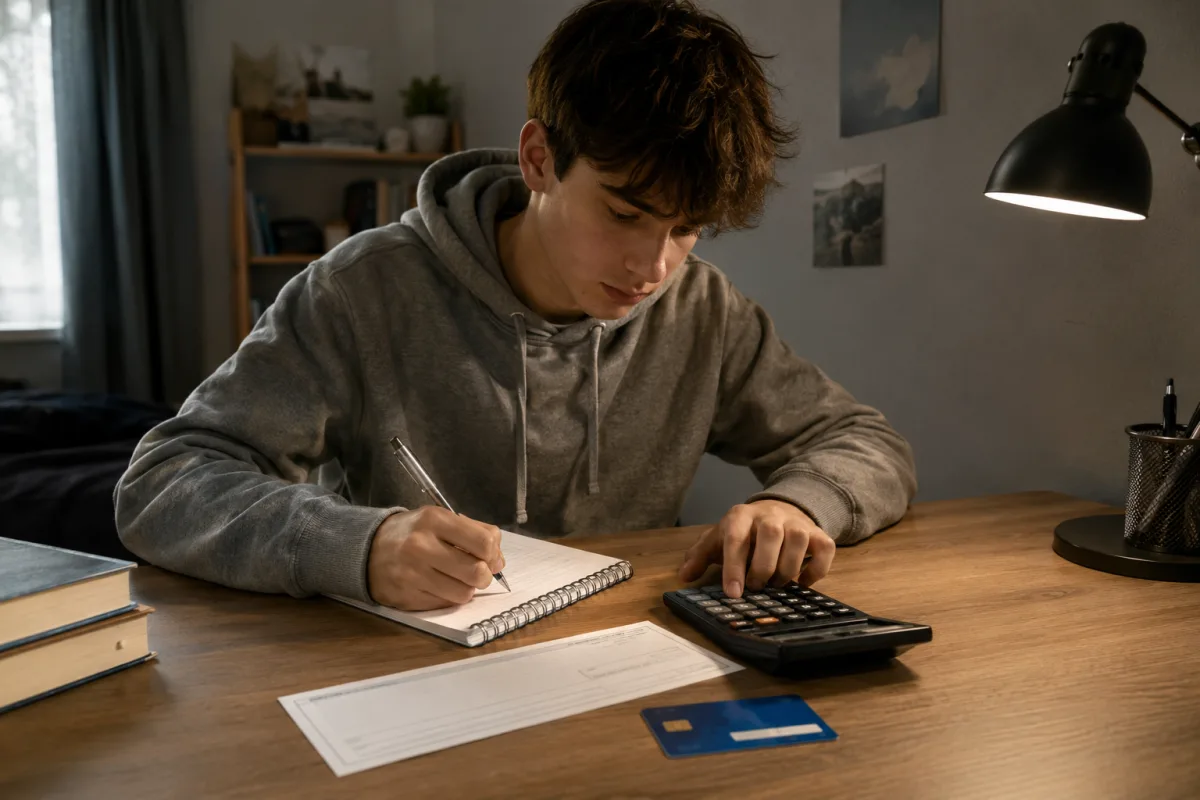

The Teen Years: Real-World Practice

Teenagers need practice with the tools of adult money: paychecks, taxes, checking accounts, debit cards, saving goals, and early credit ideas. They should understand the gap between gross pay and take-home pay before the first job, not after the first disappointing check. Use real forms when you can, including bank statements, pay stubs, mock rent, and comparison shopping, so the lessons attach to genuine paperwork rather than hypotheticals.

This is also when online scams matter most. Talk about fake job offers, prize messages, phishing links, peer-payment mistakes, and pressure to send money fast. Keep the tone practical so a teen who slips up asks for help instead of hiding it. A good habit to teach is the pause: any message that demands money urgently, promises easy pay, or asks for account details deserves a second look and, ideally, a check with a trusted adult before acting.

Make Allowance and Saving Concrete

An allowance teaches planning only when it comes with clear, steady expectations. Decide whether basic chores are simply part of family life, whether extra jobs can earn money, and what the child must cover themselves. Consistency is the lesson; if the amount swings with adult mood, it teaches uncertainty rather than management. Avoid using allowance only as reward or punishment.

Saving sticks when the goal is specific. "Save money" is vague, while "save $18 for the art set" is understandable, and a chart, jar, or balance makes progress visible. For older kids curious about how time affects money, Livecub's savings bond value guide can introduce long-horizon saving in a concrete way.

Debt, Credit, and Online Money Safety

By the teen years, explain that credit is borrowed money with rules, costs, and consequences, and that a credit card is not extra income. Interest can turn a cheap item expensive when a balance goes unpaid. Teens do not need every detail yet, but they should see that money learning continues well past graduation, through interest, insurance, and long-term saving decisions.

Digital money can feel invisible, so make it real. App purchases, saved cards, subscriptions, game currency, and one-click checkout are all genuine spending. Show how to review a cart before buying, how a free trial quietly becomes a recurring bill, and how to find and cancel a subscription that is no longer used. Sitting down together to audit the subscriptions on a family account is a concrete lesson in how small automatic charges add up over a year. Giving fits here too: keep it voluntary so the child feels ownership, and with older kids, talk about checking whether a charity or donation link is legitimate before sending anything.

Talk About Mistakes Without Shame

Kids lose cash, forget goals, chase trends, break what they bought, and compare themselves with friends. These are part of learning, and a small regret at nine, a seven-dollar mistake, is far cheaper than a seven-hundred-dollar one later. The parent's job is to set limits before the damage grows, not to rescue every choice.

When a mistake happens, reach for curiosity over criticism: "What happened?" "What would you do next time?" "Want help making a plan?" Shame makes children hide money problems, while calm questions help them think. Model your own reasoning out loud too, "we are comparing prices," "we are waiting for a sale," so kids stop inventing explanations for adult choices. Keep adult financial stress with adults; honest teaching is different from unloading fear.

Frequently Asked Questions

What age should kids learn about money?

Start with simple choices in preschool, then add saving, spending, earning, banking, and credit as the child matures.

Should allowance be tied to chores?

Families handle this differently. What matters most is keeping the rule clear so the child understands what allowance is for.

Should kids use cash or cards?

Younger children usually learn better with cash. Teens also need supervised practice with digital banking.

How do I teach a child who spends everything?

Use small goals, short waiting periods, and fixed categories, and let small regrets teach without shame.

When should teens learn about credit?

Before they can borrow. Explain interest, due dates, credit scores, and the danger of treating credit as income.

Pick one habit to make visible this week, whether it is narrating a price comparison at the store, setting up three jars, or walking a teen through a real pay stub. The goal is not a tiny financial expert but a young person who has practiced choices, patience, and caution while the stakes are still small. Those repeated ordinary moments, more than any single talk, are what carry into adulthood.

Alyssa Curlin

Edits general health, nutrition and education explainers. Medical topics are educational and link to public-health guidance.

Leave a reply

Replying to